JPMorgan Chase's Ad Move: 'Will Banks Become Media Companies?'

The Wall Street Journal got the banking world thinking big with news that JPMorgan Chase is launching an advertising arm, Chase Media Solutions, offering up deals to its banking clients from its business clients, keeping both sides of its double-sided network engaged.

Why it matters: In terms of the existing banking infrastructure, the jump from ATMs to cellphone apps shows how much the business has really changed in a short time that it took smartphones to dominate our lives.

Be smart: JPMorgan Chase has already travelled down this road, buying The Infatuation and Zagat to give its 80M customers the inside dish on restaurants, one of the places where they use credit cards most.

A "customer captivity" play: This new project is a "customer captivity" play on both sides, according to banking analysts, financial marcomms colleagues and investment bankers, and all those working in that interspace between finance and advertising. Consumers get more recommendations and discounts, like what's offered by their affinity cards, "air miles" or big business work benefits, while companies that are also bank clients get the first chance at playing inside this walled garden; both sides deepen their engagement with their bank.

Margin boost: The other upside for JPMorgan Chase, of course, is that, unlike net interest income from ordinary operations, incremental ad revenues are high-margin, additional profit.

For years, the banking sector has been looking at how to pick up the best parts of the ad ecosystem, though this is the first time one has accomplished it fully, Financial Narratives was told by Mark Boidman, Global Head of Media at Solomon Partners investment bank, author of Times Square Everywhere and Digital Sign Language.

"Ever since there have been ATMs, banks have been selling the ad space on them; now we're talking about ads on their phone apps, all of this is about harnessing those impressions," Boidman said. "Basically, if you sell toilet paper, which is a low-margin business, you'd rather be selling toilet paper with ads, because ads are 100% margin."

"With programmatic buying of ad inventory and real time bidding, this is really interesting, aggregating a mass audience, pretty powerful stuff to buy and sell traffic, and really under utilized for the size of their audience."

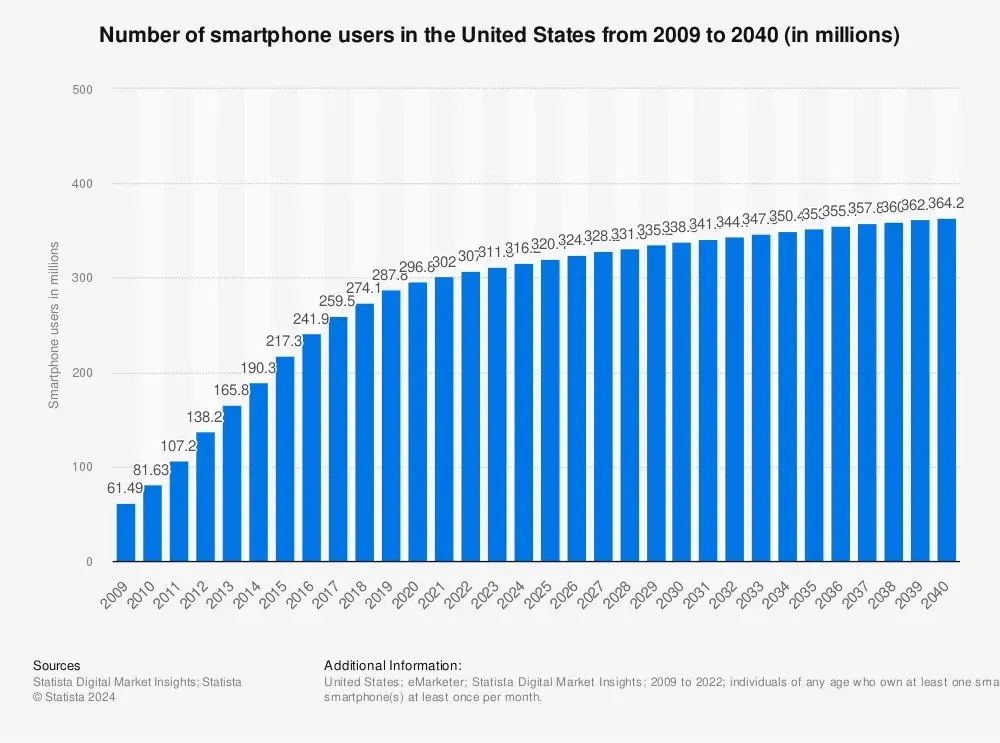

ATMs vs Smartphones: At Solomon Partners, Boidman advised on the sale of the famous digital billboards at 2 Times Square and 1600 Broadway, but thought the most interesting comparable is Cardtronics, acquired by NCR in 2021 for $2.5BN, operating the largest independent U.S. network of 70,000 ATMs. Compare that valuation for their 70,000 ATMs to JPMorgan Chase's customer base of 80,000,000, of whom the bank says 54M are already using their Chase app. We're talking a factor of nearly 1,000X more eyeballs soon.

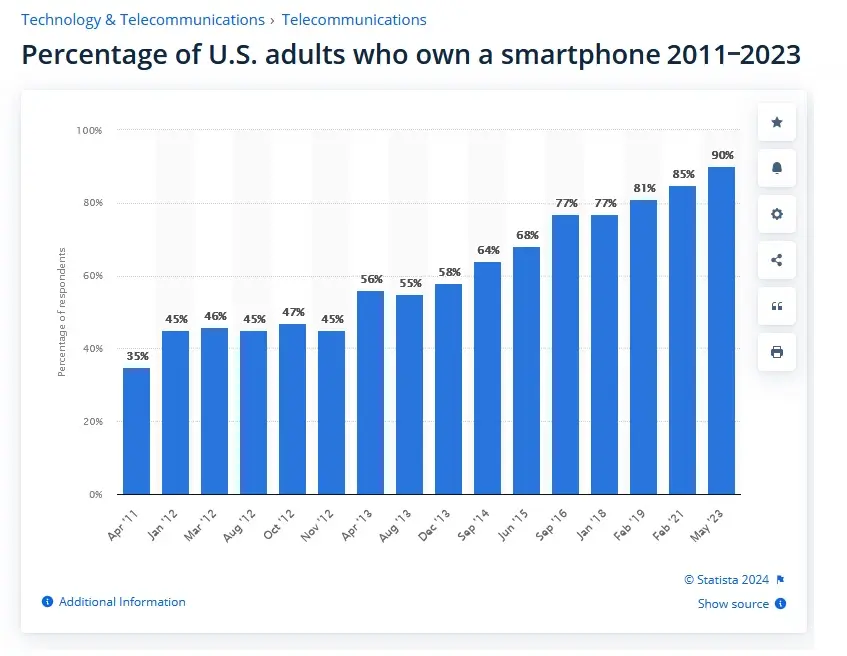

The bank has its own 16,000 ATMs and 4,700 branches. In a survey in February, it said 86% of customers prefer using the app. Nationally, 90% of U.S. adults have cellphones today, according to Statista. It's a giant market and this is one of the country's largest brands with the deepest customer base.

This app world dwarfs the retail version of in-store ads. In retail locations currently, a research report on 2024 Global Advertising Forecasts, Boidman's team cited an estimate by GroupM for these ancillary ads in stores and other locations: "Advertising spend through retail media alone was expected to reach ~$120 billion in 2023."

It's not apples-to-apples, but if there's 1 million retail stores in America versus 275 million smartphone users, the scope for this ad market the bank is targeting is tremendous.

The battle to dominate fuels the online advertisement market, and why should banks with strong mobile app footprints be any different?

Where the JPMorgan Chase deal isn't based on actually selling CPM impressions, or pay-per-click, but, rather like an affiliate program, generating a commission for a closed deal, there's a lot more at play, according to Robert Brill, CEO of digital advertising agency Brill Media, 10-time honoree across the Inc. 5000 and Financial Times 500.

"Everything is an ad network," Brill said. "Chase has masses of people using its app and website. It has customer financial data. It makes a lot of sense to monetize this opportunity. Currently, on advertising exchanges it's possible to buy data to reach people based on financial signals, such as credit payments (on time, or not), credit score, credit card usage (Visa, Mastercard, etc.), income, and lifestyle."

"This is not the first time that retailers are monetizing their attention this way. Walmart and Home Depot run ads on their websites, using consumer data to power the distribution of ads based on the product people search for," Brill said. "Where there is attention, data, and masses of people, there is opportunity to monetize with advertising," Brill reminds us.

Understanding customers via data is the long-haul plan.

The bank's long-term plan: In, 2018, already six years ago, the bank hired Professor Manuela Veloso, the head of Carnegie Mellon University’s machine learning department, to lead its artificial intelligence and machine learning research efforts.

From its perspective, this is a major step in vertical integration of their client's financial activity, one financial marcomms pro with experience told us. Speaking on the Financial Narrative 'Breaking Narratives' members-only monthly, off-the-record Zoom, the executive said the way to look at it is that payments are now an end-to-end ecosystem.

The banking giant has the clients, the merchant, the platform, the credit card, and even PayPal, whose transactions ultimately go through their system; this is a scale play.